US Dividend Tax for Korean Investors: What I Learned Collecting 1,000 Shares of QQQI

Today the dividend from my 1,000 shares of QQQI hit my account — and every time it does, I’m reminded how much understanding US dividend tax for Korean investors changed my approach to building income. Living in Korea and investing in US stocks, the tax math is genuinely friendlier than most people assume, but there’s one threshold you absolutely cannot ignore. Here’s the story of how I built this position, and the tax framework every Korea-based investor should know.

The Milestone That Started It All: 1,000 Shares of JEPI

I didn’t start with QQQI. My very first US stock position was 1,000 shares of JEPI, accumulated patiently, one block at a time.

An 18-Year Project Manager’s Approach to Investing

I spent about 18 years working as a project manager, and that career shaped how I invest more than any book ever did. As a PM, my whole job was setting clear milestones and hitting them steadily, week after week. So when I started investing, I treated it the same way: pick a concrete target — “1,000 shares” — and grind toward it consistently rather than chasing quick wins. That milestone mindset turned investing from something emotional into something methodical.

Why I Switched From JEPI to QQQI

Once I’d accumulated my 1,000 shares of JEPI, I kept studying. I came to believe QQQI — with its Nasdaq-100 focus and its income-generating covered-call structure — was a better fit for what I wanted, so I naturally transitioned over to it. Today that QQQI position has become two things at once during my parental leave: a sturdy shield for our family’s living expenses, and a powerful dollar hedge protecting us against a weakening Korean won. The monthly dividend doesn’t just feel like income; it feels like security.

How US Dividend Tax Works for Korean Investors

This is the part that surprises people. The tax treatment of US dividends for someone living in Korea is simpler — and often cheaper — than expected.

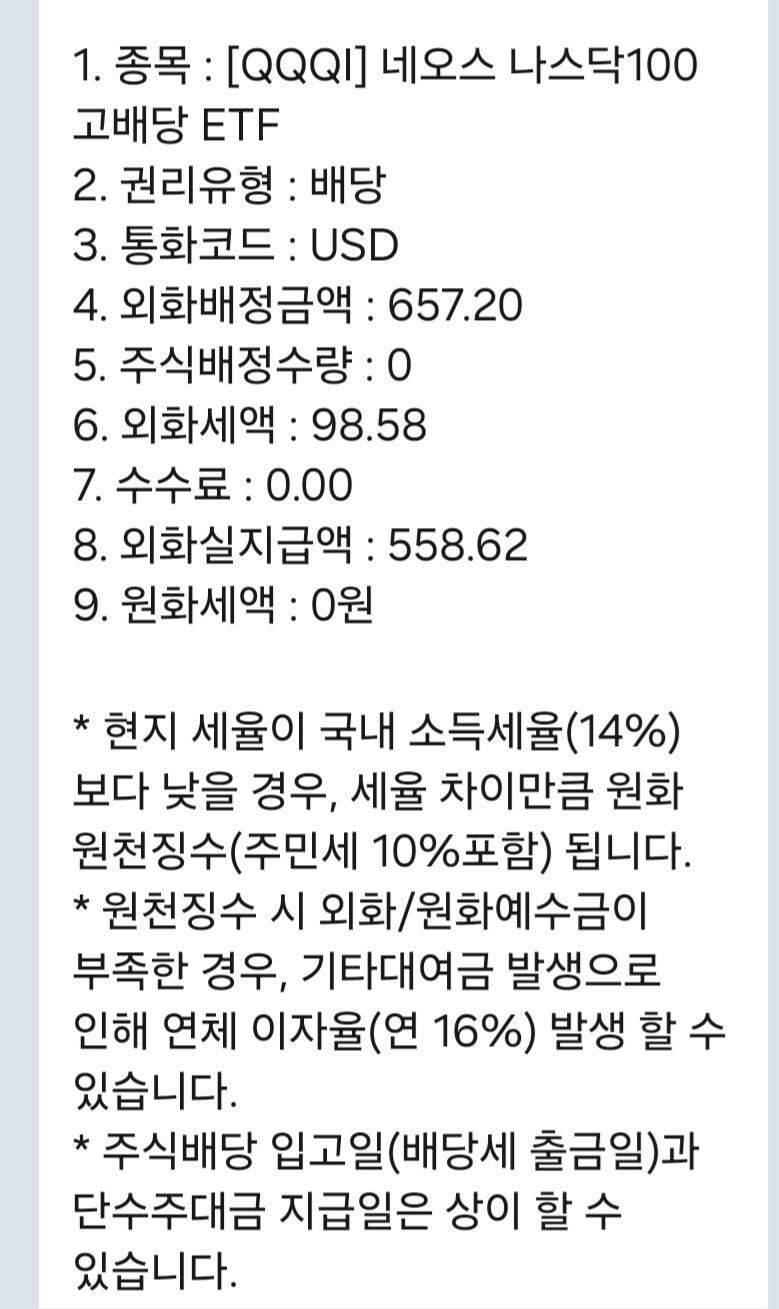

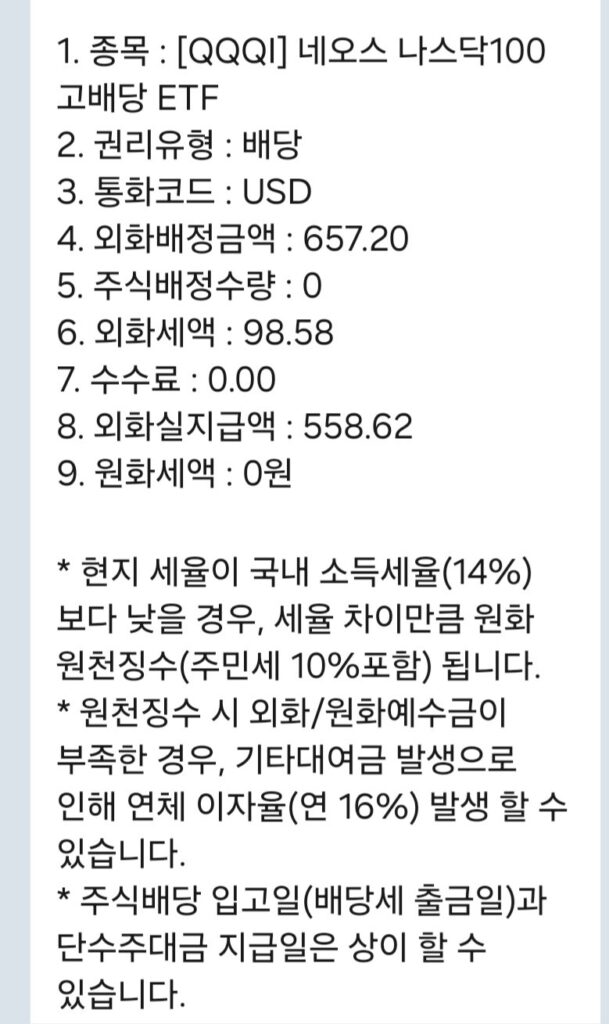

The 15% US Withholding Tax

When a US company or ETF pays a dividend to a Korean resident, the US withholds tax at the source. Thanks to the US–Korea tax treaty, that rate is 15% (rather than the default 30% that would otherwise apply). So the dividend that lands in your account has already had 15% taken off the top by the US side.

Why I Pay 0 Extra in Korea

Here’s the friendly part. In Korea, dividend income is normally taxed at a base rate of 14% (15.4% once you include the local surtax). Because the 15% already withheld in the US is higher than Korea’s 14% base rate, there is typically no additional Korean tax to pay on that dividend — the won amount withheld at home effectively comes out to zero for income under the key threshold. The foreign tax you already paid covers it. For a Korean investor in US dividend stocks, that’s a genuinely efficient setup.

The Hidden Line You Must Not Cross: 20 Million Won

Now the warning. Everything above stays clean only while your total financial income stays under one critical number.

What Happens Above ₩20 Million

In Korea, if your combined annual financial income — interest plus dividends — exceeds 20 million won (roughly $14,500), you cross into “comprehensive financial income taxation.” Below that line, your dividends are generally settled by withholding and you’re done. Above it, the excess gets stacked on top of your other income and taxed at progressive rates that climb as high as the low-to-mid 40s percent. Worse, for many people the bigger pain isn’t the income tax at all — it’s health insurance. Crossing 20 million won can trigger additional national health insurance premiums, and for those registered as dependents, it can even jeopardize that status. The health-premium hit recurs every month, which is why it stings more than a one-time tax bill.

How I Keep My Dividend Income Managed

Because of all this, keeping my annual financial income under the 20-million-won line is a core part of my strategy — not an afterthought. I actively manage the size of my dividend-generating positions and pay attention to my projected yearly total, so that I stay in the simple, withholding-only zone and avoid both comprehensive taxation and surprise health-insurance charges. When you’re investing for income rather than quick gains, protecting your net return like this matters just as much as picking the right ETF.

What This Dividend Means Right Now

Collecting that QQQI dividend today wasn’t just a number on a screen. It was proof that a slow, milestone-driven plan works. During my parental leave, that monthly distribution covers real bills and quietly defends our purchasing power against a soft won — and it does so in a tax structure I’ve deliberately kept clean and simple. The milestone mindset that served me for 18 years as a PM is now, share by share, building my family’s financial cushion.

Final Thoughts

For Korean investors, US dividends offer an appealing combination: a reasonable 15% treaty withholding, often no extra tax at home, and dollar exposure as a built-in hedge — as long as you respect the 20-million-won threshold. Build it patiently, manage the line carefully, and a dividend portfolio can become exactly what mine has: a quiet, steady shield.

Investment & Tax Disclaimer

This article reflects personal experience and opinions only. It is not financial, investment, or tax advice, and I am not a licensed financial advisor or tax professional. Tax rules — including treaty rates, the financial-income threshold, and health insurance calculations — are complex, depend heavily on your individual situation, and can change over time. The specific ETFs mentioned describe my own holdings, not recommendations, and covered-call ETFs carry their own risks including capped upside and potential erosion of principal. Past performance does not guarantee future results, and all investing carries the risk of loss, including the loss of your entire principal. Please verify current rules with Korea’s National Tax Service and consult a qualified, licensed tax professional before making any decisions.