Korean Chaebol vs US CEOs: Why I Invest More in American Stocks

One of the biggest reasons I keep the majority of my money in US stocks comes down to a single, very Korean concept: the Korean chaebol. The way companies are owned and run here — passed down through bloodlines like a family throne — is profoundly different from the professional, merit-based CEO system that powers corporate America. As an investor, that difference isn’t academic. It shapes where I’m willing to put my capital. Let me explain.

The Family Thrones: How Korea’s “Big 4” Pass Down Power

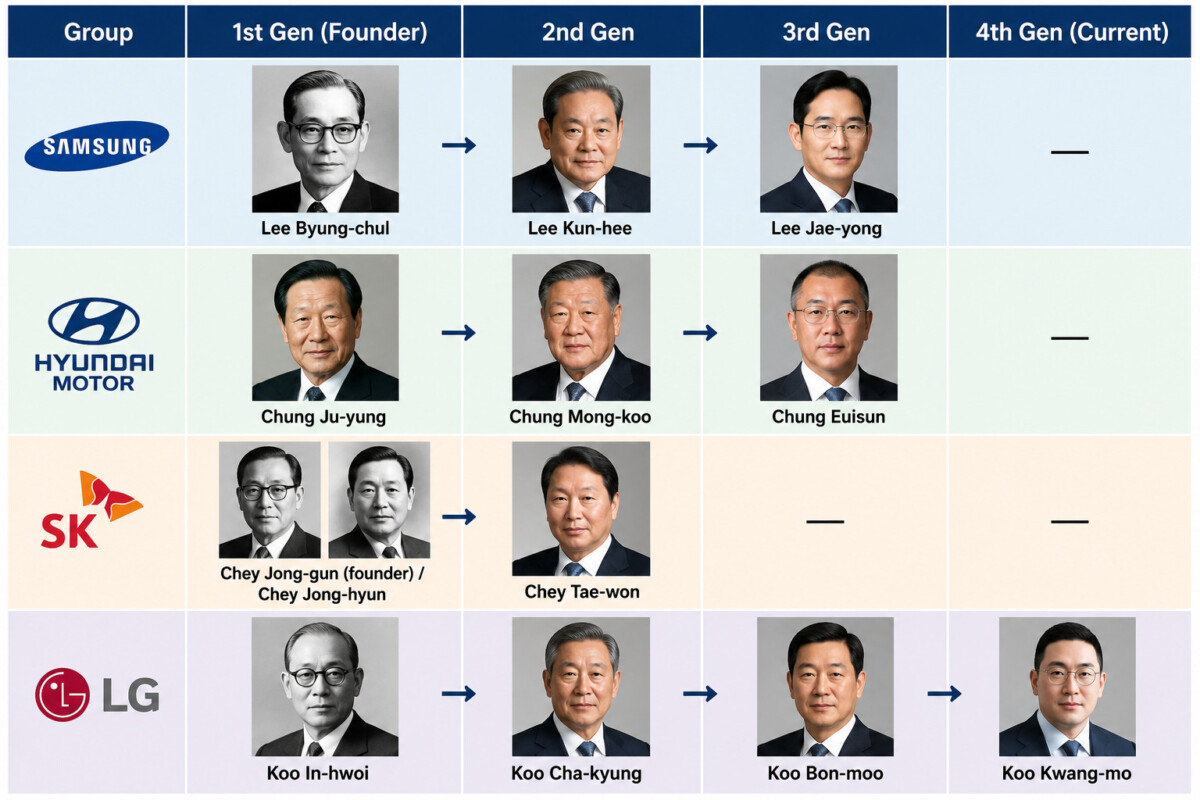

Korea’s four largest groups are all still run by the founding family, handed from one generation to the next. Here’s the lineage of power:

| Group | 1st Gen (Founder) | 2nd Gen | 3rd Gen | 4th Gen (Current) |

|---|---|---|---|---|

| Samsung | Lee Byung-chul | Lee Kun-hee | Lee Jae-yong | — |

| Hyundai Motor | Chung Ju-yung | Chung Mong-koo | Chung Euisun | — |

| SK | Chey Jong-gun (founder) / Chey Jong-hyun | Chey Tae-won | — | — |

| LG | Koo In-hwoi | Koo Cha-kyung | Koo Bon-moo | Koo Kwang-mo |

Today, Lee Jae-yong chairs Samsung, Chung Euisun chairs Hyundai Motor Group, Chey Tae-won chairs SK, and Koo Kwang-mo chairs LG. In every case, the chairman’s last name matches the founder’s. That is the chaebol system in a nutshell.

The LG Adoption Story

LG’s case is the most telling. Koo Kwang-mo is, by birth, the son of Koo Bon-moo’s younger brother — in other words, the previous chairman’s nephew. But to preserve the family’s strict tradition of eldest-son succession, he was formally adopted as Koo Bon-moo’s son so he could inherit leadership as the fourth generation. When a family will reshape its own bloodline on paper to keep the throne in the eldest male line, you understand just how deep this tradition runs.

Why Korea Runs on Chaebol Succession

So why did Korea develop this hereditary model in the first place? The answer lies in how these companies raised money and grew.

Compressed Growth and a Government-Led Economy

In the 1960s and 70s, Korea grew at breakneck speed by funneling government loans and special privileges to a handful of chosen companies. In that environment, the single most valuable weapon was the owner’s ability to make fast, bold, decisive bets — to commit a fortune to a shipyard or a chip plant overnight. That decisiveness was a genuine growth engine, and it became inseparable from one-man, owner-led control.

The Spiderweb of Circular Shareholding

For decades, Korea allowed a web-like ownership structure known as circular shareholding, in which affiliates own shares in one another. Through it, a family holding just 1–2% of a group’s total equity could still control dozens of companies. If you can command an entire empire while owning only a sliver of it, handing that control to your children becomes natural — and cheap.

Confucian Family Values

Underneath the economics sits culture. Many Koreans see a company not merely as something owned by its shareholders, but as a family legacy the clan built with its own hands. Passing it to a blood heir — especially the eldest son — was simply taken for granted.

Why America Runs on Professional CEOs

The US took a very different road, again because of how its companies were funded.

Separation of Ownership and Management

American companies went public early and pulled in enormous amounts of capital from investors around the world. In the process, the founders’ stakes were heavily diluted, and the “absolute controlling shareholder” who could run the company by personal whim largely disappeared. Ownership and management split apart.

Boards and Institutional Investors That Bite

On Wall Street, institutional investors — hedge funds, pension funds — wield serious power, and they judge management on one thing: results. If a founder’s child lacks the ability to run the company, the board and shareholders can remove them. Leadership is a job you can be fired from, not a birthright.

Brutal Estate Taxes and a Culture of Giving

The US also levies heavy estate taxes, which makes handing a company intact to one’s children structurally difficult. That’s part of why figures like Bill Gates and Warren Buffett chose to give their fortunes to charitable foundations and leave the running of business to capable professionals.

The Core Difference

Here’s the contrast in one line: in Korea, a controlling family can command the entire board and all the affiliates while owning only a tiny stake. In America, even a celebrated CEO is essentially a hired manager, fully accountable to the board and shareholders. One system rewards bloodline; the other, at least in theory, rewards performance.

Why This Makes Me Lean Toward US Stocks

This is where it becomes an investment thesis for me. When I buy a US stock, I’m betting that the most capable person available will be running the company — and that if they fail, they’ll be replaced. Look at who leads the most valuable companies in the world right now: Jensen Huang, a self-made immigrant engineer, built Nvidia. Elon Musk runs Tesla and SpaceX on the strength of his own ventures. And while the whole world knows Steve Jobs, almost no one can name his children — because Apple didn’t pass to his bloodline. It went to Tim Cook, a professional operator chosen on merit.

That’s the kind of structure I want my money inside: one where leadership is earned, scrutinized, and replaceable. To be fair, the chaebol model gave Korea decades of bold, fast growth that a committee might never have dared, and these groups remain formidable. But as a shareholder, I sleep better owning companies where the next leader is chosen for being the best, not for being born first.

Final Thoughts

The gap between the Korean chaebol and the American CEO system isn’t a story of good versus bad — it’s the product of two very different histories: Korea’s need for an owner’s decisive breakthroughs, and America’s highly developed capital markets with their relentless shareholder checks. Understanding that difference is, for me, one of the clearest reasons to keep tilting my portfolio toward the US.

Investment Disclaimer

This article reflects personal opinions and observations only. It is not financial, investment, tax, or legal advice, and I am not a licensed financial advisor. Governance structure is just one of many factors that affect a company’s performance, and neither professional management nor family ownership guarantees good results — well-run family businesses and poorly-run professionally-managed ones both exist. Past performance does not guarantee future results, and all investing carries the risk of loss, including the loss of your entire principal. Please do your own research and consult a qualified, licensed professional before making any investment decision.