Tier 3 US Stock Portfolio Allocation: How I Built a Core-and-Satellite Portfolio in Percentages

During my parental leave, I finally had the time to study companies properly and rethink my whole approach to investing. The result is a deliberate US stock portfolio allocation built around one idea: a fortress-like core that won’t crumble in a crash, surrounded by smaller satellite bets on the future. In this post I’ll break the whole thing down in percentages — no won amounts, just the ratios — so you can see the structure rather than the size.

A quick note before the breakdown: about 80% of my total holdings are in US stocks (held in dollars) and roughly 20% are in Korean stocks (held in won). Everything below describes the US portion — the 80% — and the percentages are shares of that US portfolio.

My Top-Level Split: 80% US, 20% Korea

I’m a Korean investor, but I keep the overwhelming majority of my capital in US equities. The 80/20 split isn’t an accident. Holding most of my assets in dollar-denominated US stocks gives me currency diversification away from the won and exposure to what I consider the most reliably upward-trending market in the world. The 20% in Korean stocks keeps me connected to my home market. With that frame set, here’s how the US 80% is actually arranged.

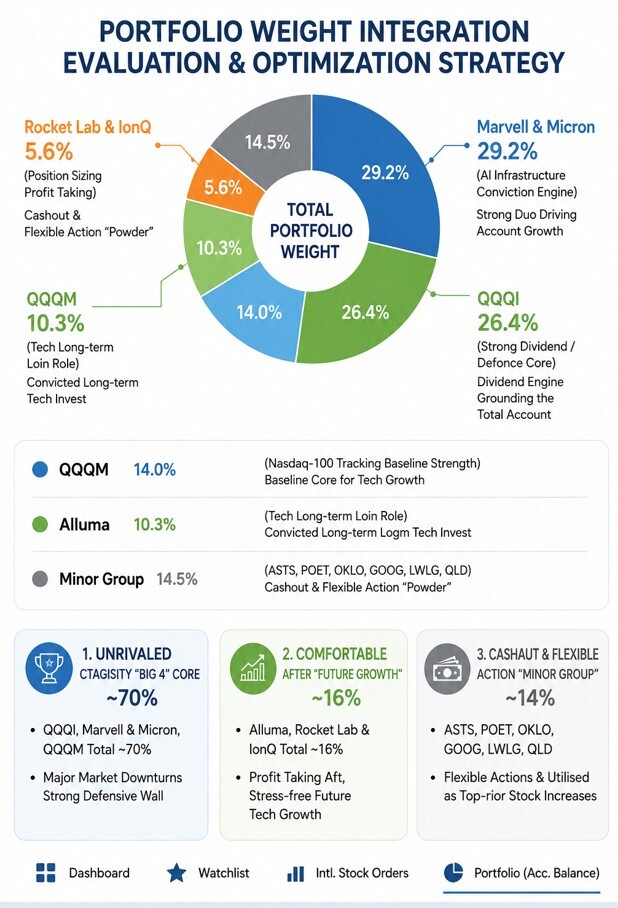

Tier 1: The “Big 4” Core (~70% of My US Portfolio)

The top four positions make up roughly 70% of my US holdings. This is the wall. Even in a brutal sell-off, having this much weight in resilient, high-quality names means the whole account doesn’t collapse.

Income and Index ETFs as My “Cash” (~41%)

Two of my four core positions are ETFs, and together they’re around 41% of the US portfolio:

- QQQI — about 27%. This income-focused covered-call ETF is the single largest position and the anchor of the entire account, throwing off steady monthly distributions.

- QQQM — about 14%. A low-cost Nasdaq-100 index ETF that gives the portfolio its baseline fitness and broad market exposure.

Here’s a key part of my philosophy: I treat these ETF positions almost like cash. I keep them at a steady target ratio rather than trading in and out of them, so they act as both ballast and dry powder.

My AI Infrastructure Two-Top: Marvell & Micron (~29%)

The other half of the core is conviction, not ballast. Marvell and Micron together make up roughly 29% (very loosely 14–15% each). These are my AI-infrastructure bets — the engines meant to drive the account’s growth as demand for AI chips and memory keeps climbing. Pairing them gives me concentrated exposure to the AI buildout without betting everything on a single name.

Put the ETFs and the two-top together and you get that ~70% core: a structure designed so that “even in most crashes, the account survives.”

Tier 2: Future Growth Satellites (~16%)

This is where I let myself dream a little — but with position sizes small enough that I can sleep at night.

- My highest-conviction individual growth stock — about 10%. (Editor’s note: this is the position you referred to as “앨루마” — please confirm the exact ticker so I can name it correctly.) This is a technology name I hold for the long term out of belief in its engineering, and it plays the “midfield” role in the portfolio.

- Rocket Lab — about 3% and IonQ — about 3%. I trimmed both by taking profits, so they’re now small enough that even a 10%+ swing barely dents the overall account. That’s the point: I can watch frontier innovation in space and quantum computing play out with zero stress, because the downside is capped by sizing.

Tier 3: The Flexible Tail (~14%)

The bottom group is built for optionality. It includes AST SpaceMobile (ASTS), POET Technologies (POET), Oklo (OKLO), Alphabet/Google (GOOGL), Lightwave Logic (LWLG), and ProShares Ultra QQQ (QLD) — each roughly 1–3% of the US portfolio.

Some of these are swing-trade targets (POET, OKLO) and some are cash-out candidates (LWLG, ASTS). They’re intentionally small, which makes them easy to trim into cash whenever I want — or to use as “ammunition” to build up a blue-chip position like Google later on. Low weight, high flexibility.

From ETF Beginner to Stock Picker: My Investing Philosophy

The structure above didn’t appear overnight. It’s the product of how my approach evolved.

Three Years of ETFs First

For my first three years in US stocks, I bought almost nothing but ETFs — SCHD, JEPQ, QQQ, and VOO. I didn’t have the time or knowledge to analyze individual companies, so I let broad, proven funds do the work while I learned. That foundation is the single best decision I made as a beginner.

Why I Treat ETFs Like Cash

Now that parental leave has given me real time to study businesses, I’ve added individual stocks — but I never abandoned the ETFs. I hold QQQI and QQQM at a steady ratio and mentally file them as “cash.” They give me income, stability, and a reserve I can lean on, which in turn frees me to take measured risks in the satellite tiers. My underlying belief is simple and, I admit, optimistic: if you invest in genuinely good companies, US stocks tend to trend upward over time. The core-and-satellite structure is how I try to stay invested in that idea without betting the farm.

Final Thoughts

A good US stock portfolio allocation, to me, isn’t about picking one perfect stock — it’s about architecture. A ~70% fortress core, a ~16% growth layer sized so volatility can’t hurt me, and a ~14% flexible tail I can reshape at will. Add the 80/20 split between US and Korean markets on top, and I have a structure I can hold through almost anything while I keep learning.

Investment Disclaimer

This article describes my own portfolio and opinions for illustration only. It is not financial, investment, tax, or legal advice, and I am not a licensed financial advisor. The tickers and allocations mentioned are not recommendations to buy or sell, and a concentrated portfolio like mine (with ~70% in just four positions) carries significant concentration risk. The belief that “good companies always go up” is a personal conviction, not a guarantee — markets can and do fall, individual stocks can go to zero, and covered-call ETFs carry their own risks including capped upside and potential erosion of principal. Past performance does not guarantee future results, and all investing carries the risk of loss, including the loss of your entire principal. Please do your own research and consult a qualified, licensed professional before making any investment decision.