Parental Leave in Korea: How a Dad of Three Is Studying Investing to Buy His Freedom

Since April 1st, I’ve been on parental leave in Korea from my German company — a father of three (two daughters and a son) stepping away from the office to be home with my family. On paper it sounds simple. In reality, taking leave as a man in Korea is a quiet act of rebellion, and it pushed me to do something I’d put off for years: seriously study investing and the path to financial freedom.

This is the honest story of the numbers behind my year off, the social stigma that comes with it, and why I’m spending these months learning how money works.

The Reality of Parental Leave in Korea for Fathers

Korea is famous for two things that sit in painful contradiction: an obsession with family, and the lowest birth rate in the world. The government keeps building policies to encourage parents to have children and take leave. The culture, though, hasn’t caught up.

A Country With the World’s Lowest Birth Rate

Korea has been wrestling with a record-low fertility rate for years, and the government has rolled out benefit after benefit to reverse it. Parental leave pay, childcare subsidies, incentives — the institutional support genuinely exists. The problem isn’t really the policy on paper. It’s what happens to you at work when you actually use it.

The Stigma Men Still Face

Here’s the uncomfortable truth most foreigners don’t hear about. When a man in Korea takes parental leave, he often quietly braces for consequences: being passed over for promotion, or being nudged toward “voluntary” resignation when he returns. The system says “please take leave.” The unwritten workplace culture says “if you do, don’t expect your career to survive it.” That gap between policy and reality is, in my opinion, one of the real reasons Korea’s birth rate stays so low — the rules changed faster than the mindset did, and culture always needs more time to follow.

I won’t pretend I’m immune to this. I applied for my year of leave already expecting to leave the company afterward. For me, this isn’t a pause in my career so much as a deliberate exit ramp — and that reframing is exactly why the financial planning mattered so much.

The Math Behind My One-Year Plan

If I was going to take a year off — possibly my last year of stable employment — I couldn’t do it on hope. I had to know the numbers worked. So I built a plan where multiple income streams cover our family’s minimum cost of living for twelve months.

Our Family’s Cost of Living

With three kids, our household spends at minimum about 5,000,000 KRW a month (roughly $3,600). That’s the floor I had to cover, every month, no excuses. For a one-income family on leave, that number is intimidating — so I attacked it from several directions at once.

Building Income Pipelines With Dividend ETFs

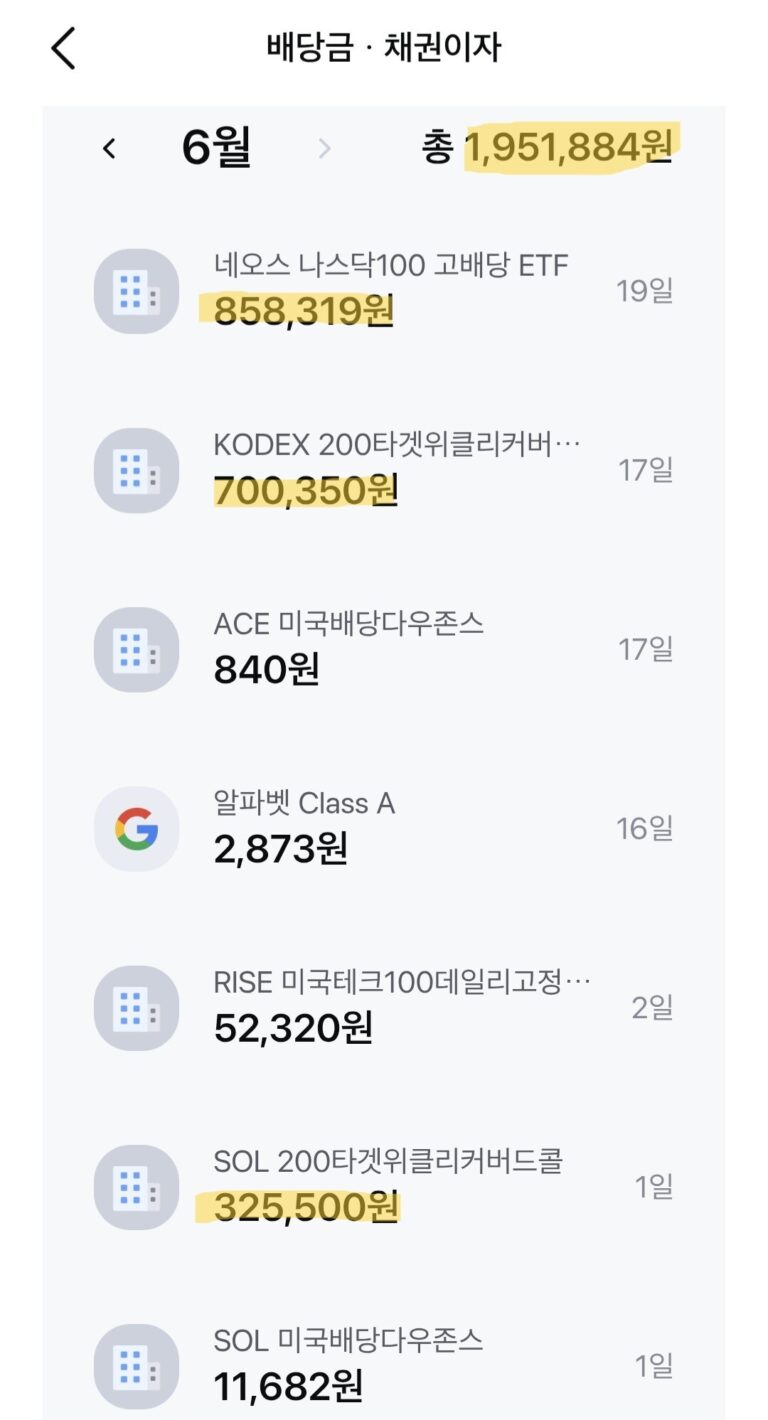

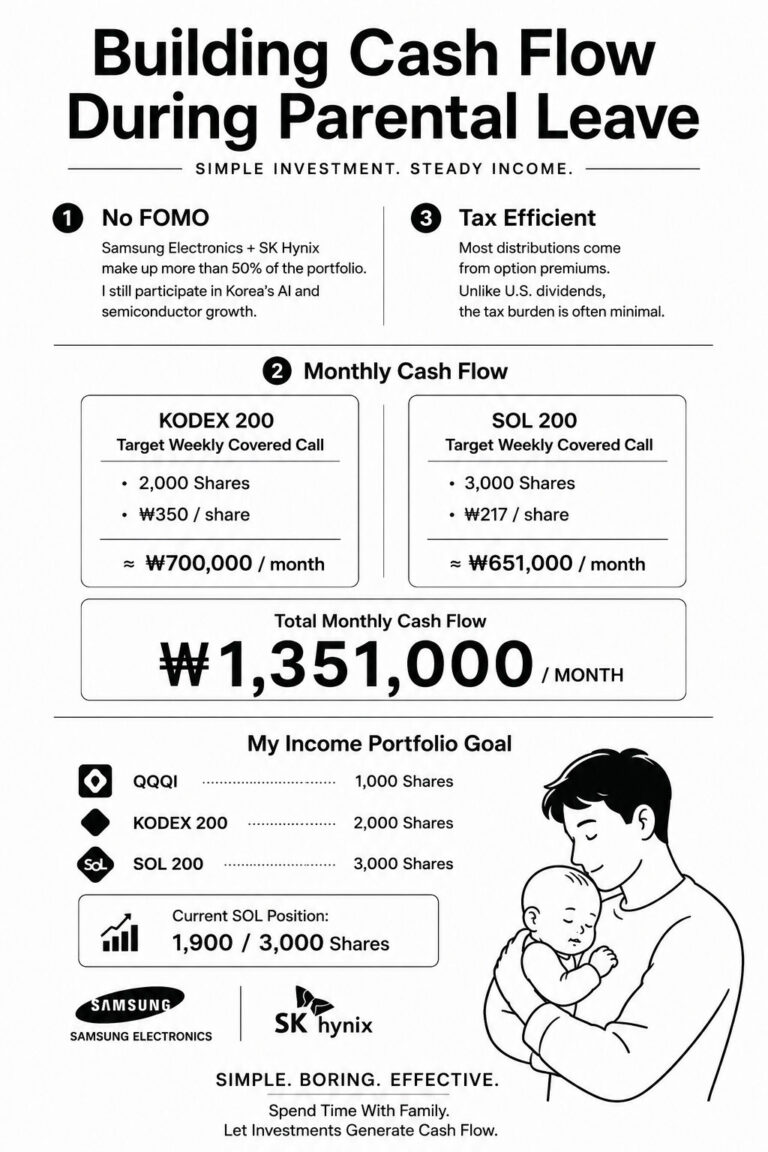

The piece I’m proudest of is the cash flow I built myself. Using income-focused covered-call ETFs — QQQI in the US market and a Korea-listed Kodex 200 Target Weekly Covered Call product — I constructed a pipeline generating roughly 2,000,000 KRW (about $1,450) in monthly distributions. Covered-call ETFs trade away some long-term upside in exchange for steady monthly income, which is exactly the trade-off that suits someone who needs predictable cash flow during a leave year. (They carry their own risks, which I’ll come back to.)

Government Benefits, My Wife’s Income, and Side Hustles

On top of that pipeline, the rest of the plan stacks up like this:

- Government parental leave pay (in my case): about 2,500,000 KRW/month for months 1–3, 2,000,000 KRW for months 4–6, and 1,600,000 KRW for months 7–12.

- My wife’s part-time work: an extra 1,500,000 KRW (about $1,100) a month.

- My side income: roughly 500,000 KRW (about $360) a month from blogging and small freelance work.

Add it all together and even in the leanest stretch — months 7 through 12, when the government benefit is lowest — the combined streams still clear our 5,000,000 KRW floor. For one full year, our family’s minimum living costs are covered. That security is what lets me breathe and think clearly about what comes next.

Why I’m Really Studying Investing

The leave isn’t just about being present for my kids, though that’s the heart of it. It’s also the runway for a bigger goal: building enough financial independence that my income no longer depends on a company that may not reward me for prioritizing my family.

Policy Is Ahead of Culture — So I’m Planning Around It

I’ve made peace with the fact that I can’t single-handedly fix Korea’s workplace culture. What I can do is refuse to let a slow-moving culture dictate my family’s future. If the social cost of taking leave is real, then the smartest response is to reduce my dependence on that system entirely. That’s why I’m pouring my free hours into studying economics, markets, and cash flow.

Turning Leave Into a Launchpad

So these months have become a strange kind of gift. While I’m changing diapers and reading bedtime stories, I’m also rebuilding how I think about money — moving from “trade my time for a salary” toward “build assets that pay me whether or not I show up to an office.” A scary career situation became the push I needed to take ownership of my financial life.

Final Thoughts

Parental leave in Korea, for a father, is still an act that requires courage and a backup plan. I chose to treat mine as both a chance to be there for my three kids and a deadline to get serious about financial freedom. The culture may take another generation to fully accept dads like me. I’m not waiting around for permission — I’m building the numbers that let me decide for myself.

Investment Disclaimer

This article reflects personal experiences and opinions only. It is not financial, investment, tax, or legal advice, and I am not a licensed financial advisor. The specific ETFs and income strategies mentioned describe my own situation and are not recommendations. Covered-call and high-yield ETFs in particular carry meaningful risks — including capped upside, potential erosion of principal, and distributions that can fall or be partly a return of capital — and relying on them for living expenses can be risky if markets turn. Government benefit amounts vary by individual circumstances and change over time, so verify your own eligibility with official sources. Past performance does not guarantee future results, and all investing carries the risk of loss, including the loss of your entire principal. Please do your own research and consult a qualified, licensed professional before making any financial decision.