Monthly Dividend Income Update: How $1,330 a Month Is Funding My Second Life

This June, my monthly dividend income climbed to roughly $1,330 — close to 2 million Korean won (at about 1,500 won to the dollar). That number might not sound life-changing on its own, but for me, three months into parental leave, it crossed a quiet but enormous threshold: between my dividends, my government parental-leave pay, and a little side income, my family’s living expenses are now comfortably covered. And that has me thinking about something I once only dreamed of — a second life. Here’s exactly how I got here.

The Milestone: A Three-Legged Stool That Covers Our Life

For the first time, my income isn’t a single salary — it’s a three-legged stool. Leg one is my dividend income. Leg two is the parental-leave benefit the government pays. Leg three is modest side income from things like blogging. Stacked together, they now meet our household’s minimum cost of living without strain.

Here’s the thought that keeps me up (in a good way): I have nine months of leave left. If I can build just one more meaningful side-income stream during that time — on top of what I already earn — then quitting my company and starting a genuine “second life” stops being a fantasy and becomes a plan. The dividends are the foundation that makes that math even thinkable.

My 3 Dividend Engines

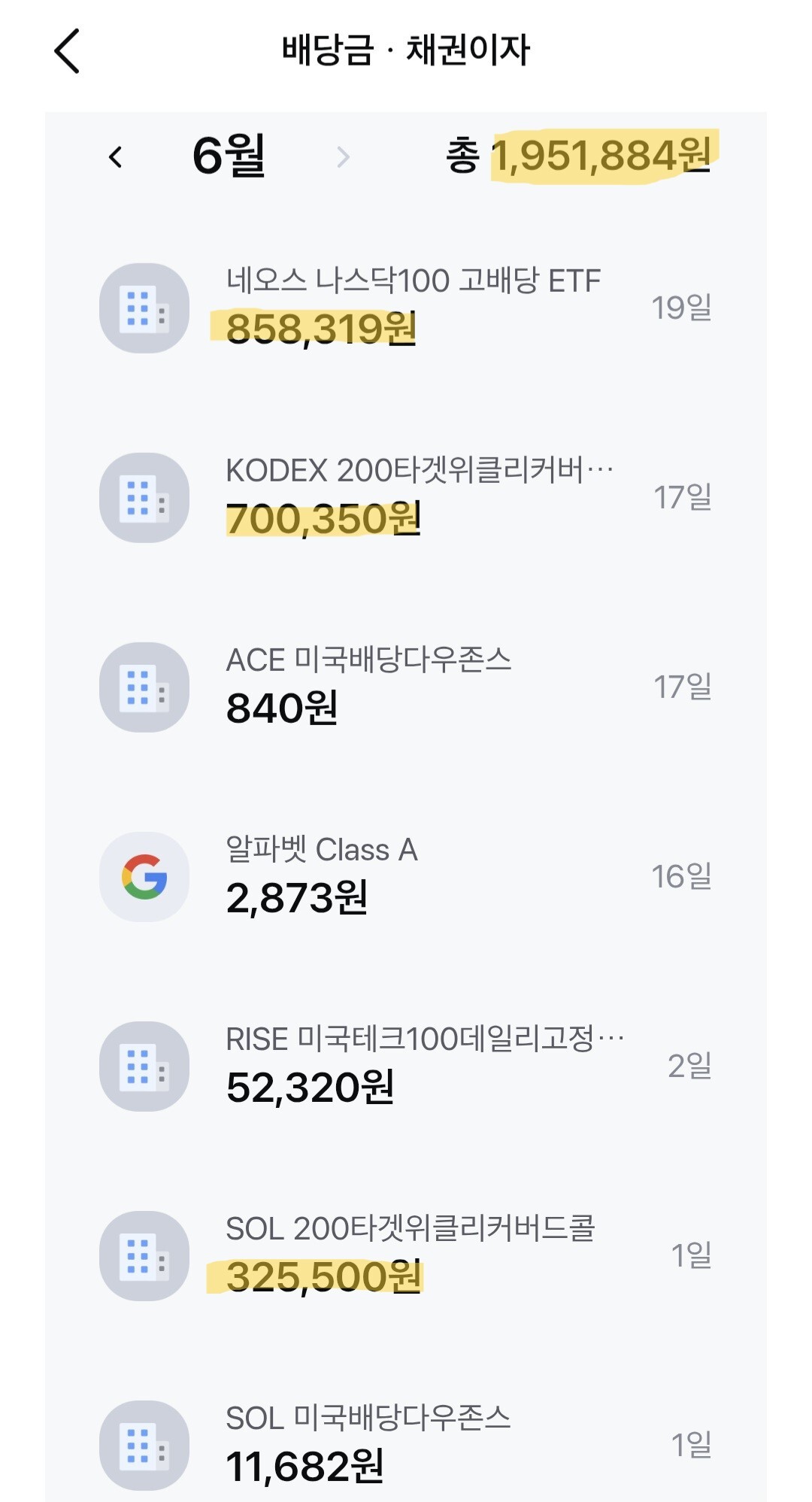

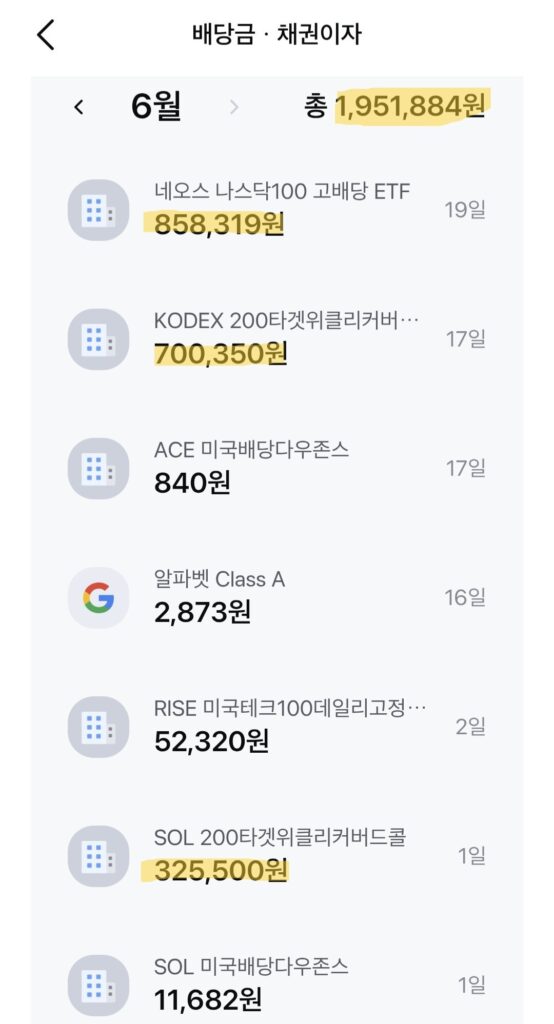

All of that ~$1,330 a month comes from just three holdings. Here’s the breakdown, in dollars.

QQQI — 1,000 Shares, About $565/Month

My biggest engine is QQQI, the income-focused Nasdaq-100 covered-call ETF I spent a long time accumulating. My 1,000 shares now throw off about $565 a month — the single largest piece of my dividend income, and the anchor of the whole structure. Reaching that 1,000-share milestone was one of my proudest investing achievements.

KODEX 200 Target Weekly Covered Call — 2,000 Shares, About $465/Month

Next is KODEX 200 Target Weekly Covered Call, a Korea-listed ETF that tracks the KOSPI 200 and sells weekly call options for income. My 2,000 shares produce roughly $465 a month. I’d set 2,000 shares as my target, and I hit it.

SOL 200 Target Weekly Covered Call — Growing From 1,500 to 2,171 Shares, About $300/Month

The third engine is SOL 200 Target Weekly Covered Call, a similar weekly covered-call fund from a different provider. At the start of June I held 1,500 shares, which paid me about $213. Since then I’ve grown the position to 2,171 shares, so this month I expect around $300. This is the leg I’m still actively building.

Add the three together — about $565 + $465 + $300 — and you land right around $1,330 a month in dividend income, paid out month after month.

Why I Keep Buying SOL on Every Dip — Until KOSPI 10,000

SOL is the position I’m not done with. My plan is simple: every time the price dips, I just keep accumulating — all the way until the KOSPI crosses 10,000. As long as Korea’s index is grinding toward that milestone with the occasional pullback, I treat each dip as a chance to add shares and grow this income leg a little more. It’s a milestone-driven accumulation strategy, the same patient approach that built my QQQI and KODEX positions.

The Tax Edge That Makes This Work

Here’s the part that makes the Korean covered-call ETFs especially powerful for me. Both KODEX and SOL pay large distributions, but a big advantage is that the option-premium portion of those distributions is tax-exempt in Korea. That means my real tax burden on this income is small.

Crucially, it also means these distributions barely move me toward Korea’s 20-million-won financial-income threshold — the line where comprehensive income taxation and extra health-insurance charges kick in. Because so much of the payout is tax-free, I can collect a lot of cash before that ceiling becomes a concern. So for now, my plan is straightforward: keep filling the gap in my monthly cash flow with these three holdings, efficiently and with minimal tax drag.

The Bigger Picture: Building Toward a Second Life

Three months ago, taking leave felt like a financial leap of faith. Today, the spreadsheet says the leap is landing. The dividends cover a real, recurring chunk of our life; the leave pay and side income handle the rest. If I can add one more income source over the next nine months, the door to leaving corporate life and designing my own days swings open. That’s the second life I’m quietly building toward — one dividend at a time.

Final Thoughts

A $1,330 monthly dividend income won’t make anyone a tycoon. But as a steady, mostly tax-efficient stream that covers real expenses while I’m home with my kids, it’s doing exactly what I designed it to do. I’ll keep stacking shares, keep hunting for that next income stream, and keep documenting the journey honestly — the good months and the rough ones alike.

Investment & Tax Disclaimer

This article reflects personal experience and opinions only. It is not financial, investment, or tax advice, and I am not a licensed financial advisor or tax professional. The distribution figures are based on recent payouts and will vary month to month; covered-call ETFs carry real risks, including capped upside, variable distributions, and loss of principal if the underlying index falls — relying on variable income to cover living expenses can be risky if markets turn. Tax treatment depends on your individual circumstances and can change; verify with Korea’s National Tax Service and a qualified professional. Past performance does not guarantee future results, and all investing carries the risk of loss, including the loss of your entire principal. Please do your own research before investing.