Samsung Q2 Earnings Hit a Record — So Why Did the Stock Fall?

Samsung Q2 earnings just delivered one of the most stunning numbers in the company’s history, and yet Samsung Electronics shares are falling today. If that sounds contradictory, you’re not alone in being confused — this is exactly the kind of “great news, falling stock” moment that trips up investors everywhere, and it’s worth unpacking carefully, especially since it tells us something important about where Micron might be headed too.

https://www.etnews.com/20260707000014

Samsung Q2 Earnings: The Numbers Behind the Record

On July 7, 2026, Samsung Electronics disclosed preliminary consolidated results for the second quarter: 171 trillion won in revenue and 89.4 trillion won in operating profit — both the highest quarterly figures in the company’s history. To put that operating profit number in perspective, it’s up 56.21% from the prior quarter’s 57.23 trillion won, and an almost unbelievable 1,810% higher than the same quarter last year, when the semiconductor division was still working through a down-cycle. Revenue climbed 27.74% quarter-over-quarter and 129.31% year-over-year. For the first half of 2026 combined, Samsung’s cumulative revenue reached 304.87 trillion won (up 98.34% year-over-year) with operating profit of 146.63 trillion won — more than twelve times what it earned in the first half of last year. This is, by any measure, one of the great earnings turnarounds in Samsung’s history, powered almost entirely by the memory chip recovery and surging AI-driven demand.

Why Samsung’s Stock Fell Despite Record Earnings

So why is the stock down? A few distinct forces are tangled together here, and separating them matters.

Profit-Taking After a Massive Run-Up

The simplest explanation is the oldest one in markets: “buy the rumor, sell the news.” Samsung shares had already run up enormously in anticipation of a strong report, and record-breaking results that essentially matched what investors expected gave many traders an obvious moment to lock in gains. A pullback right after a blowout report — even a record one — is a classic pattern when a stock has already priced in most of the good news.

Performance-Bonus Provisions Trimmed the Headline Number

There’s a company-specific wrinkle too. Ahead of the report, several brokerages had actually cut their operating-profit forecasts for Samsung — not because the underlying chip business was weakening, but because Samsung was expected to book larger-than-anticipated employee performance-bonus provisions in Q2, after some of that expense wasn’t reflected in Q1. Analysts were explicit that this was a timing and accounting issue, not a sign of deteriorating fundamentals, and most maintained bullish, “top pick” ratings on the stock even as they trimmed near-term estimates.

Lingering Fear From Meta’s Cloud Pivot

Samsung’s stock had also already broken below the psychologically important 300,000 won level earlier in the week, driven by a very different story: a wave of reports that Meta plans to pivot from purely buying AI computing power to also leasing out its own data-center capacity, which stoked fears of an AI infrastructure spending slowdown. That selloff hit Samsung and SK Hynix together, and some of that nervousness appears to still be lingering into today’s earnings reaction, layering on top of the profit-taking.

What Analysts Say Actually Matters (and What Doesn’t)

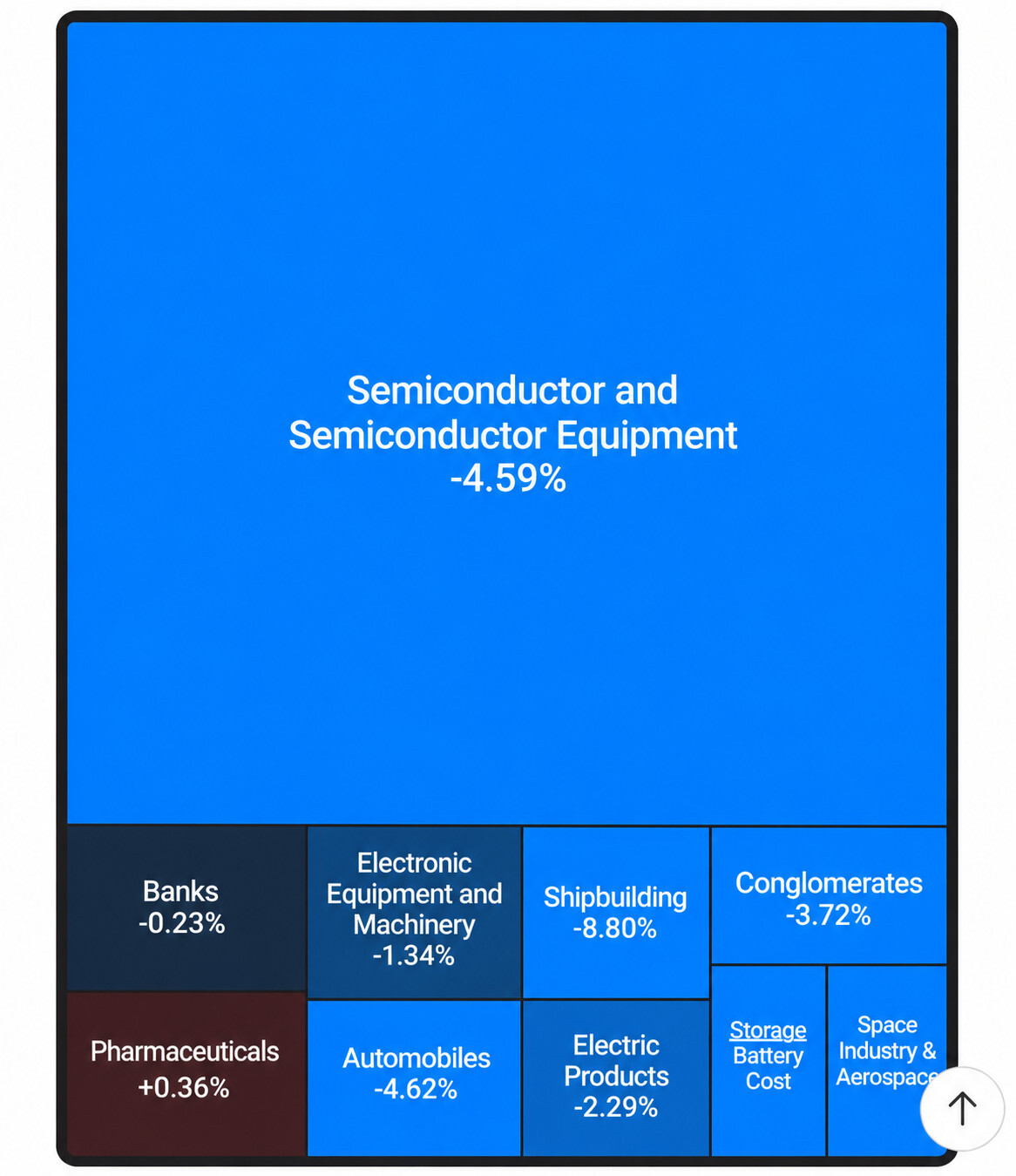

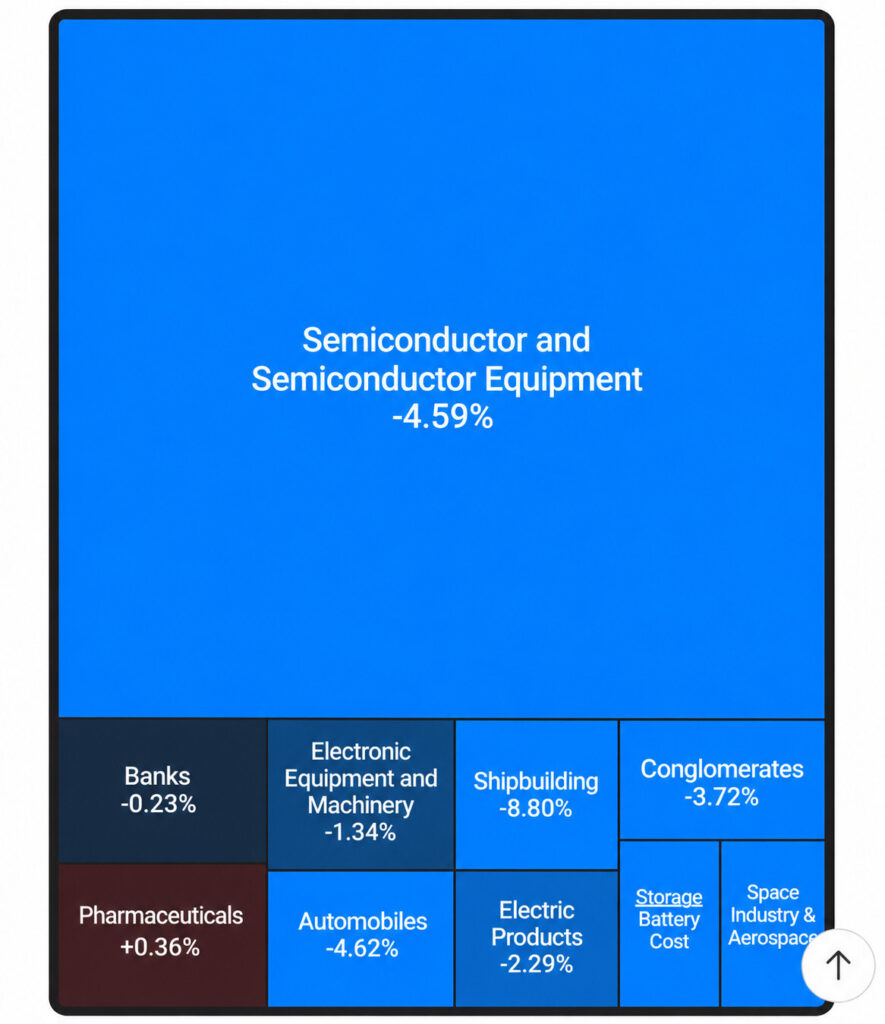

Here’s the important distinction Korean brokerages have been drawing, and I think it’s the right one: the Meta headline and the bonus-provision accounting are noise layered on top of the real signal. What would actually damage the memory thesis is a pullback in hyperscaler capex, shrinking long-term HBM supply contracts, cooling server DRAM prices, or falling next-generation GPU orders — and none of those have actually shown up. Generic DRAM and NAND prices, in fact, rose 58% and 75% quarter-over-quarter respectively, comfortably beating expectations. Samsung’s memory bottleneck, if anything, is translating directly into surging profitability.

What Samsung Q2 Earnings Mean for Micron

This is the part I think matters most for anyone holding US memory stocks. Samsung, SK Hynix, and Micron increasingly move as a connected trade — and Samsung’s numbers today are a strong signal for Micron specifically.

Korean analysts pointed out that, based on Micron’s own recent results and guidance, its operating margin has already climbed above 80%, with Japan’s Kioxia guiding to a similarly extraordinary 74.3% operating margin for the same quarter. The read is straightforward: the global memory bottleneck is lifting profitability across every major producer simultaneously, not just Samsung. If Samsung’s blowout quarter confirms that DRAM and NAND pricing power remains this strong industry-wide, it reinforces the bull case for Micron heading into its own next earnings report — because the same supply-demand tightness driving Samsung’s 1,810% profit surge is the same tightness Micron has been selling into.

Analysts do flag one thing worth watching: as HBM and enterprise SSD market-share competition heats up in the second half, alongside rising concerns about Chinese memory makers gaining share, volatility across all three companies’ stocks could increase even if the underlying earnings trend stays strong. Strong fundamentals and a choppy stock price can coexist — which is exactly what’s happening to Samsung today.

Final Thoughts

Samsung Q2 earnings were, by the numbers, spectacular — a record quarter that confirms the memory supercycle is real and accelerating. The stock’s drop today isn’t a verdict on that story; it’s a mix of profit-taking, a one-off accounting item, and lingering jitters from unrelated tech-sector headlines. For Micron watchers, the message from Samsung’s results is reassuring: the pricing power and margin expansion happening in Korea’s memory sector appears to be an industry-wide phenomenon, not a company-specific story.

Investment Disclaimer

This article reflects personal opinions and analysis based on publicly reported information. It is not financial, investment, tax, or legal advice, and I am not a licensed financial advisor. Preliminary earnings figures are subject to revision when final results are released later this month, and stock price reactions can shift quickly based on factors unrelated to fundamentals. Nothing here is a recommendation to buy or sell any security. Past performance does not guarantee future results, and all investing carries the risk of loss, including the loss of your entire principal. Please do your own research and consult a qualified, licensed professional before making any investment decision.