Micron Stock: Why I’m Buying Every Dip Despite the Noise

Micron stock has been on a wild ride this week, and I want to lay out exactly why I’m not scared of it — I’m buying it. Shares fell more than 10% intraday yesterday, on top of a sharp drop just days earlier. But when I strip away the headlines and look at what actually matters, my conviction hasn’t wavered one bit. This is my personal take, not a recommendation, but I think it’s worth sharing honestly.

https://www.sec.gov/ix?doc=/Archives/edgar/data/0000723125/000072312526000015/mu-20260528.htm

The Fact: Micron’s Q3 Earnings Were a Genuine Record

Let’s start with what’s indisputable. On June 24, Micron reported fiscal Q3 2026 results that blew past every expectation:

- Revenue: $41.46 billion — up roughly 346% year over year.

- Non-GAAP EPS: $25.11 — well above the roughly $20.49 analysts had modeled.

- Gross margin: 84.9% — a massive jump from around 45% in the same quarter a year earlier.

This wasn’t a modest beat. It was one of the most dramatic earnings surprises I’ve seen from a large-cap semiconductor company, driven by explosive demand for high-bandwidth memory (HBM) feeding the AI buildout. That’s fact, not opinion — and it’s the foundation of my entire Micron stock thesis.

Why Micron Stock Dropped Anyway

Here’s the part that confuses a lot of people: if the earnings were this strong, why did Micron stock fall so hard right after?

The Apple Price-Hike Headline

Just a day after the blowout report, Apple announced it was raising prices on Macs and iPads, explicitly citing surging memory-chip costs. Apple shares fell over 6% on the news, and the reversal dragged Micron and the broader chip sector down with it. The narrative shifted overnight from “Micron is printing money” to “Micron’s pricing power is now hurting consumers and other tech companies.”

The Meta Cloud-Pivot Headline

Then, just days later, reports emerged that Meta plans to pivot from being a pure buyer of AI computing power into a provider — leasing out cloud capacity and competing with AWS, Azure, and Google Cloud. That single report sparked fears of an AI computing oversupply, and memory and optical-communication stocks were hit across the board: Micron fell nearly 10%, Marvell over 7%, and several other AI infrastructure names dropped even harder.

My View: This Is Noise, Not a Change in the Fundamentals

Here’s my honest take, and I want to be clear this is purely my personal opinion. Neither of those two headlines changes the actual thing that matters for Micron stock: how much memory the world needs for AI, and how much Micron is selling and earning from it.

Apple raising prices because memory costs are rising is, if anything, confirmation of Micron’s pricing power — not a threat to it. And whether Meta becomes a cloud provider or stays a pure buyer, the underlying AI training and inference workloads still require enormous amounts of memory. What would actually change my thesis is Micron’s own revenue or profit turning down. Everything else — a competitor’s strategic pivot, a customer’s pricing decision — is noise layered on top of the real signal.

Why I Keep Buying the Dip

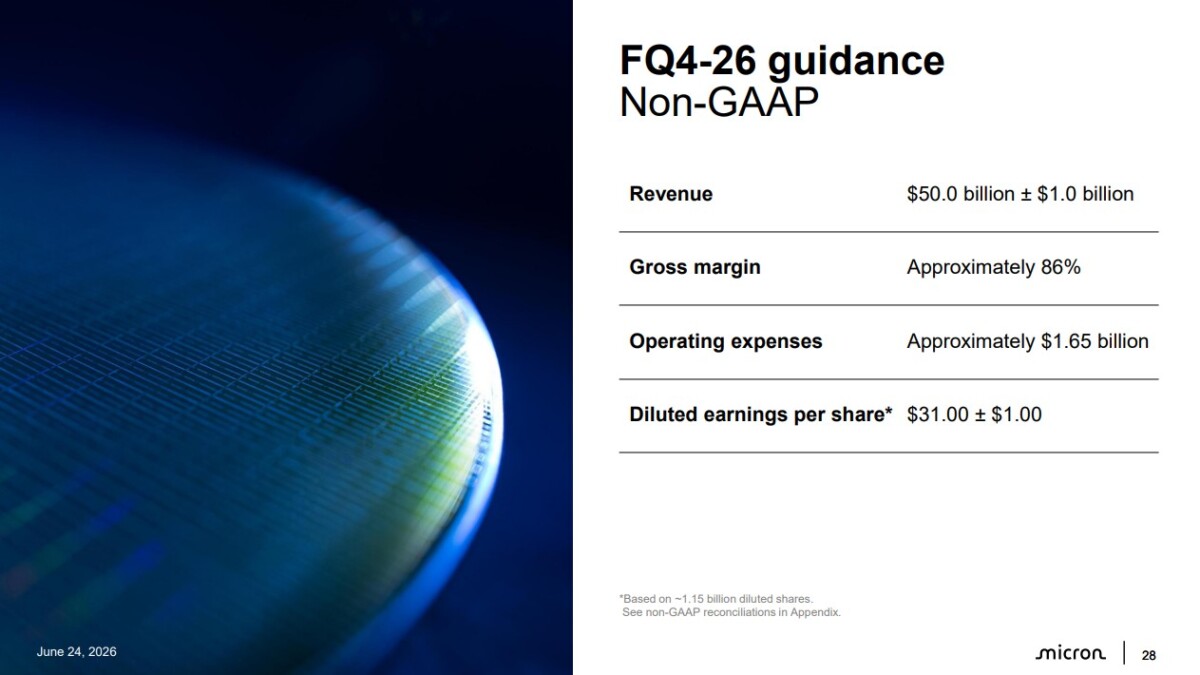

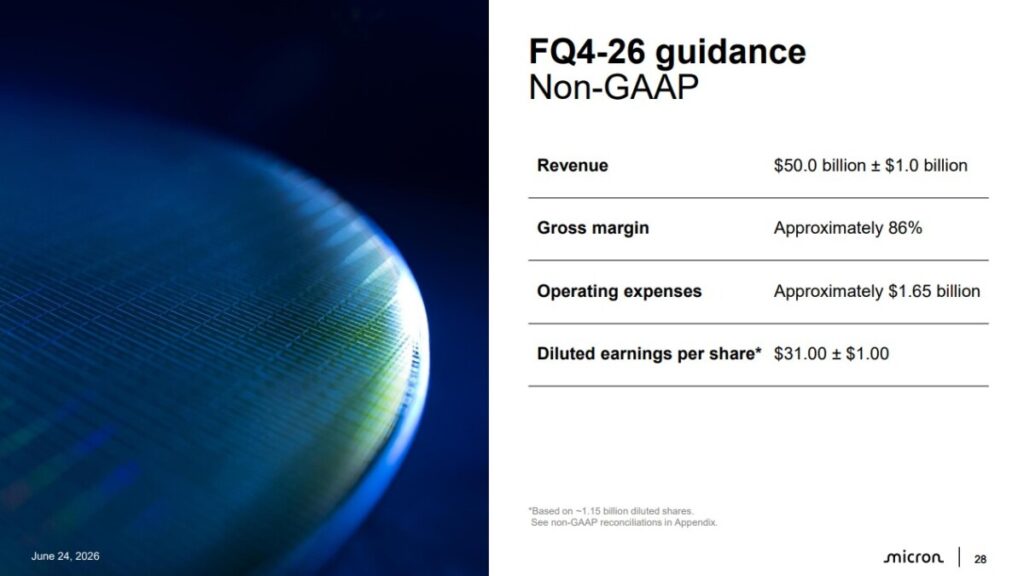

So my approach is simple and, frankly, a little stubborn: as long as Micron’s revenue and earnings keep climbing, I keep buying Micron stock on every dip, headlines be damned. The company itself isn’t just riding a temporary wave — it guided for next quarter’s revenue at roughly $50 billion, up from $11.3 billion a year earlier, and management has described the current supply shortage as structural, with Micron able to fill only about half to two-thirds of customer demand for HBM. That’s not the profile of a fading cycle; it’s the profile of a company that can’t make chips fast enough.

The Next Catalyst: Samsung’s Earnings on July 7

There’s one more reason I’m watching closely right now. Samsung Electronics is expected to release preliminary guidance for its second-quarter 2026 results around July 7, with the full earnings report following later in the month. Since Samsung, SK Hynix, and Micron together make up the global memory oligopoly, Samsung’s numbers will be an important cross-check on everything Micron just told us. If Samsung’s memory business confirms the same strength — rising prices, tight HBM supply, strong AI-driven demand — it reinforces the case that this is an industry-wide structural shift, not a Micron-specific story. I’ll be watching that report as closely as I watched Micron’s.

The Bottom Line: Watch Revenue, Ignore the Noise

My rule for this whole memory-chip cycle is straightforward: I’ll keep buying Micron stock on weakness as long as revenue and profit keep growing. The day that trend actually reverses — not a headline about a competitor, not a price hike at Apple, but Micron’s own numbers rolling over — is the day I’ll reconsider. Until then, I see every double-digit pullback as an opportunity, not a warning sign.

Final Thoughts

Markets often confuse noise for signal, especially in a stock as volatile as Micron has been this year. Apple’s pricing decisions and Meta’s cloud ambitions make for dramatic headlines, but they don’t change how much memory AI infrastructure actually consumes. That’s the number I’m watching — and as long as it keeps climbing, I’m keeping my buy orders in.

Investment Disclaimer

This article reflects my personal opinions and speculation only. It is not financial, investment, tax, or legal advice, and I am not a licensed financial advisor. “Buying the dip” carries real risk — a stock can continue falling, and a thesis can be wrong. Nothing here is a recommendation to buy or sell any security. Past performance does not guarantee future results, and all investing carries the risk of loss, including the loss of your entire principal. Please do your own research and consult a qualified, licensed professional before making any investment decision.