QQQI ETF: How I Reached 1,000 Shares and Built My Monthly Income Machine

This June, I watched my brokerage app show a number I’d been working toward for almost a year: 1,000 shares of the QQQI ETF. My average cost is $51.68, the price sits around $54.69, and the position now generates roughly $550 a month in passive income after tax. But the number on the screen is only half the story. The real story is how I got here — a deliberate switch, a project manager’s discipline, and a mindset shift that made the whole thing surprisingly stress-free. Let me share it.

The Switch: Why I Sold All My JEPQ for QQQI

My income journey didn’t start with QQQI. Last August, I sold my entire JEPQ position and began steadily moving the money into QQQI instead. The reason was simple: QQQI’s yield was running somewhat higher than JEPQ’s, and for a portfolio built around generating monthly cash flow, that edge mattered. Both are excellent Nasdaq-100 covered-call income funds, but once I’d done the homework, QQQI was the better fit for my specific goal. So I made the switch and never looked back.

Hitting the 1,000-Share Milestone (A Project Manager’s Way to Invest)

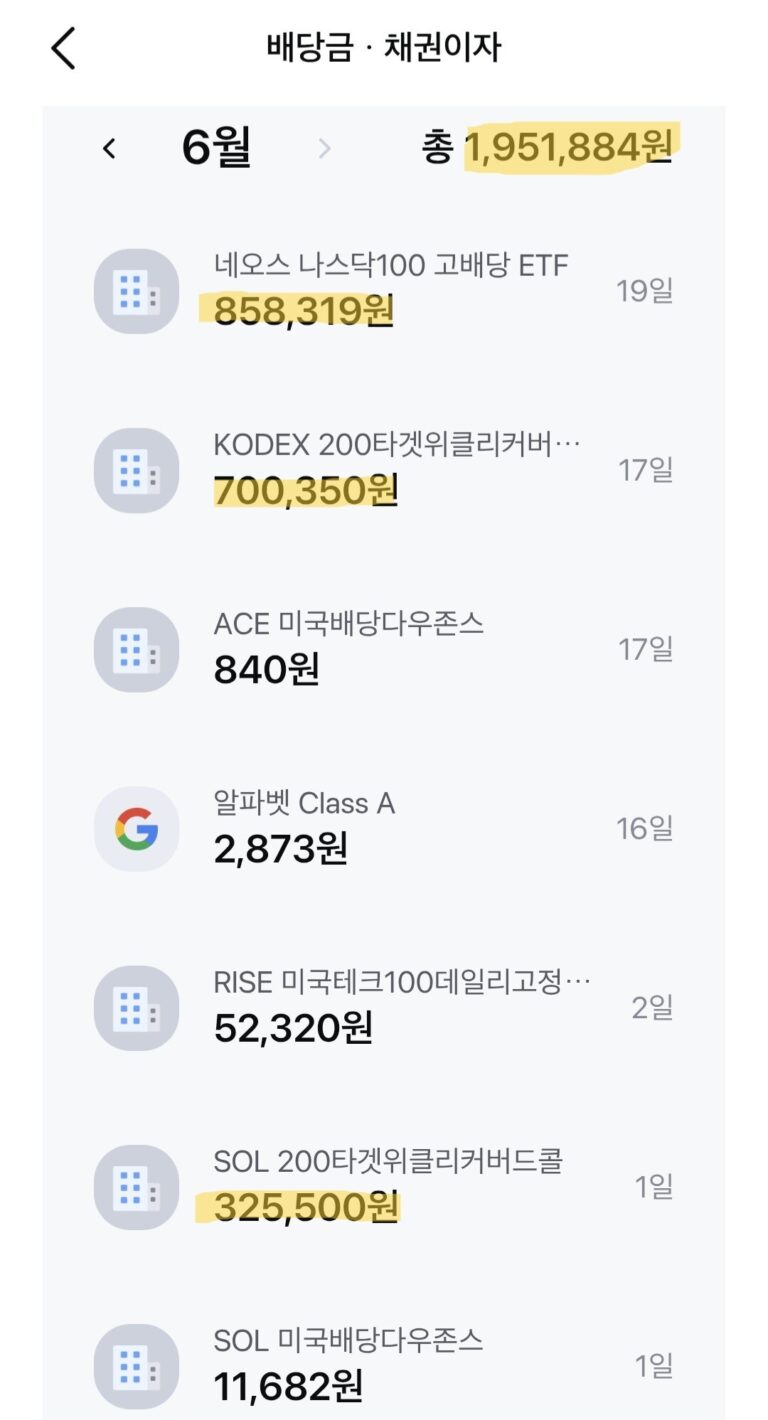

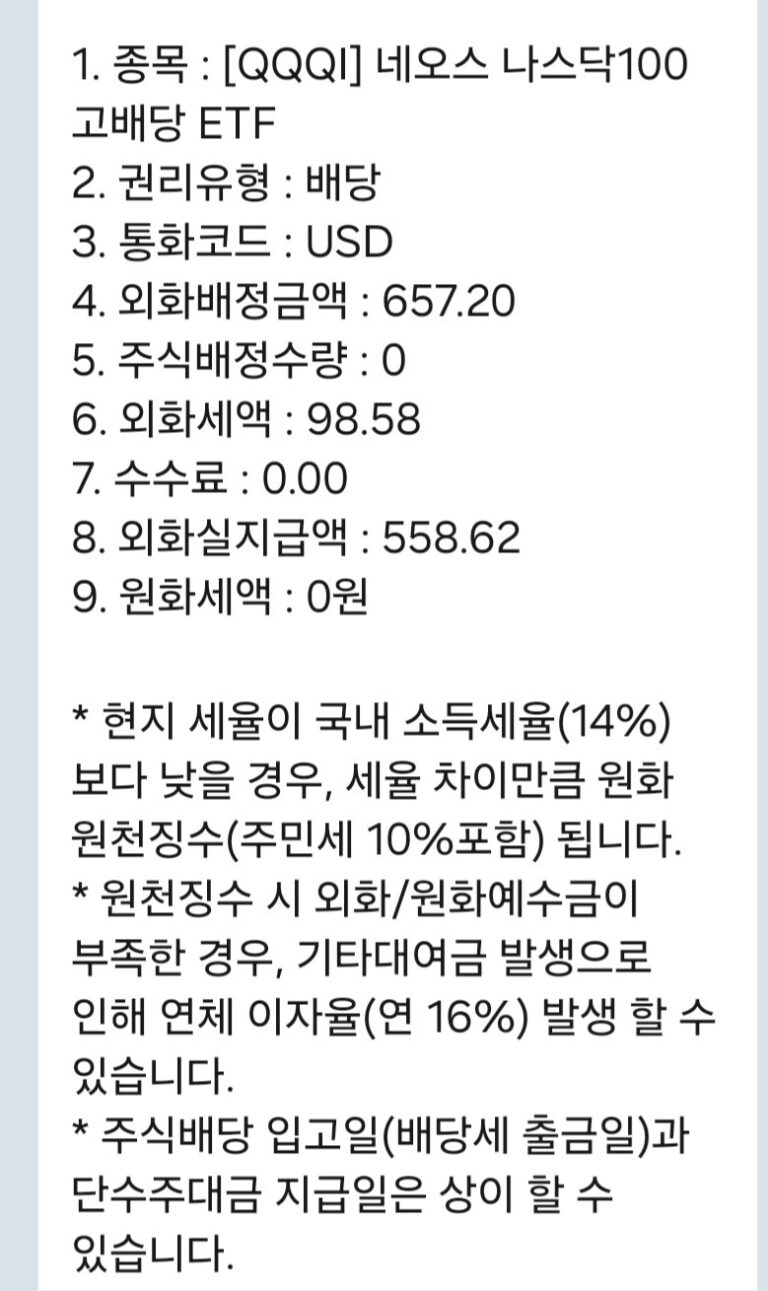

Here’s where my background shows. I spent about 18 years as a project manager, and that career rewired how I do everything — including investing. A PM doesn’t drift toward vague goals; a PM sets a concrete, measurable target and grinds toward it, milestone by milestone. So instead of thinking in fuzzy dollar amounts, I set a clean target: 1,000 shares of QQQI. I dollar-cost-averaged in, block by block, month after month — and in June, I hit it. That single milestone now pays me about $550 every month (after the 15% dividend withholding), like clockwork.

The Returns: 6% in Dollars, Nearly 10% With the Won Tailwind

This is one of my favorite parts, and it’s a uniquely Korean-investor angle. In pure dollar terms, my QQQI position is up about 6% (from $51.68 to roughly $54.69). But my actual return, measured in Korean won, is closer to 9.84% — because the won has weakened against the dollar since I bought in. The currency move quietly added several extra points of return on top of the fund’s own performance.

That’s exactly why I love holding US dollar assets from Korea: I get the fund’s income and a built-in hedge against a softening won. People love to point out that covered-call ETFs have “capped upside.” Fair enough. But between the monthly distributions I’ve already collected, the ones still to come, and that currency tailwind, I’m deeply grateful for this kind of return. Capped upside looks very different when the downside is cushioned and the cash keeps flowing.

Why Covered-Call Income Feels Different

The biggest thing I’ve learned holding QQQI is emotional, not financial: a dividend that lands every single month brings a kind of calm that a regular growth stock never gave me. During my parental leave, when there’s no salary hitting the account, that steady rhythm of income is genuinely grounding. It’s come to feel like a golden goose — a position I only ever want to feed.

I’ll be honest about the caveat, because I always am: I know full well that no investment is truly immune to loss, and a covered-call ETF can decline if the underlying market falls. “An investment that can’t lose” doesn’t really exist. But within a diversified plan, QQQI has become the steady, income-producing core that lets me take measured risks elsewhere — and that role is worth a great deal to me right now.

The Psychology: I Only Ever Think About Buying

Here’s the mindset shift that surprised me most. With most stocks, I’m constantly running the mental math of when to sell — locking in gains, trimming, managing the exit. With QQQI, I simply don’t think about selling at all. I only think about buying more. And that one change makes investing easy. There’s no agonizing over the perfect exit, no second-guessing — just a calm, repeatable habit of accumulation. When the only decision is “add more when I can,” stacking shares becomes natural and almost effortless. For a tired parent on leave who wants simplicity, that psychological ease is its own kind of return.

What This Means for My Parental Leave

Stepping back, this 1,000-share milestone isn’t just a personal scoreboard. It’s one solid leg of the income that’s covering my family’s life while I’m home with my kids, free from a salary. Building it the slow, boring, milestone-driven way — the same way I once ran projects — is what turned a leap of faith into something that actually works. QQQI is the quiet engine humming in the background while I focus on what matters most.

Final Thoughts

The QQQI ETF taught me that the most powerful investing isn’t always the most exciting. A clear target, patient accumulation, a currency tailwind, and a mindset that only ever says “buy more” combined to build a monthly income machine I’m genuinely proud of. I’ll keep feeding the goose — one share at a time.

Investment & Tax Disclaimer

This article reflects personal experience and opinions only. It is not financial, investment, or tax advice, and I am not a licensed financial advisor. No investment is free from the risk of loss — covered-call ETFs in particular carry real risks including capped upside in rising markets, variable distributions, and erosion of principal if the underlying index falls, and currency moves can reverse and work against you just as easily as for you. The figures describe my own position, not a recommendation. Past performance does not guarantee future results, and all investing carries the risk of loss, including the loss of your entire principal. Please do your own research and consult a qualified, licensed professional before investing.