Korean Covered Call ETFs: Why I’m Building Monthly Income During Parental Leave – 3 Reasons

During my parental leave, I’m quietly building a monthly cash-flow machine using two Korean covered call ETFs: KODEX 200 Target Weekly Covered Call and SOL 200 Target Weekly Covered Call. While I keep most of my money in US stocks, these two are the heart of my Korean (won-denominated) allocation — and for three very specific reasons, they’re perfect for a parent on leave who needs steady income without stress. Let me walk you through exactly why.

https://www.samsungfund.com/eng/etf/product/view.do?id=2ETFP4

(KODEX 200 Target Weekly Covered Call Homepage – ENG version)

What These Two Korean Covered Call ETFs Actually Are

Both funds track the KOSPI 200 — Korea’s blue-chip index — while running a weekly covered-call strategy on top. In plain terms, they sell short-dated (one-week) call options on the index and collect the option premium, which they pay out to investors as monthly distributions. Both target a 15% annual premium and, crucially, they’re the “target” type: they dynamically adjust how much of the index they sell calls against, so unlike old-school covered-call funds that cap nearly all your upside, these let you keep some of the market’s gains while still harvesting income. That single design choice is what makes them work for me.

Reason 1: No FOMO, Because Samsung and SK Hynix Are Built In

The first reason is psychological, and it’s bigger than it sounds. Samsung Electronics and SK Hynix now make up more than half of the KOSPI 200. Since these ETFs track that index, owning them means I’m automatically riding the same AI-memory rally that’s been driving Korea’s market to record highs.

That matters because it kills my fear of missing out. If I held a pure income fund with no exposure to those two giants, I’d feel sick watching them soar while I sat on the sidelines. Instead, the “target” covered-call structure lets me capture a meaningful slice of that upside and get paid every month. I’m not choosing between growth and income — I’m getting a measured dose of both.

Reason 2: Steady Cash Distributions Every Month

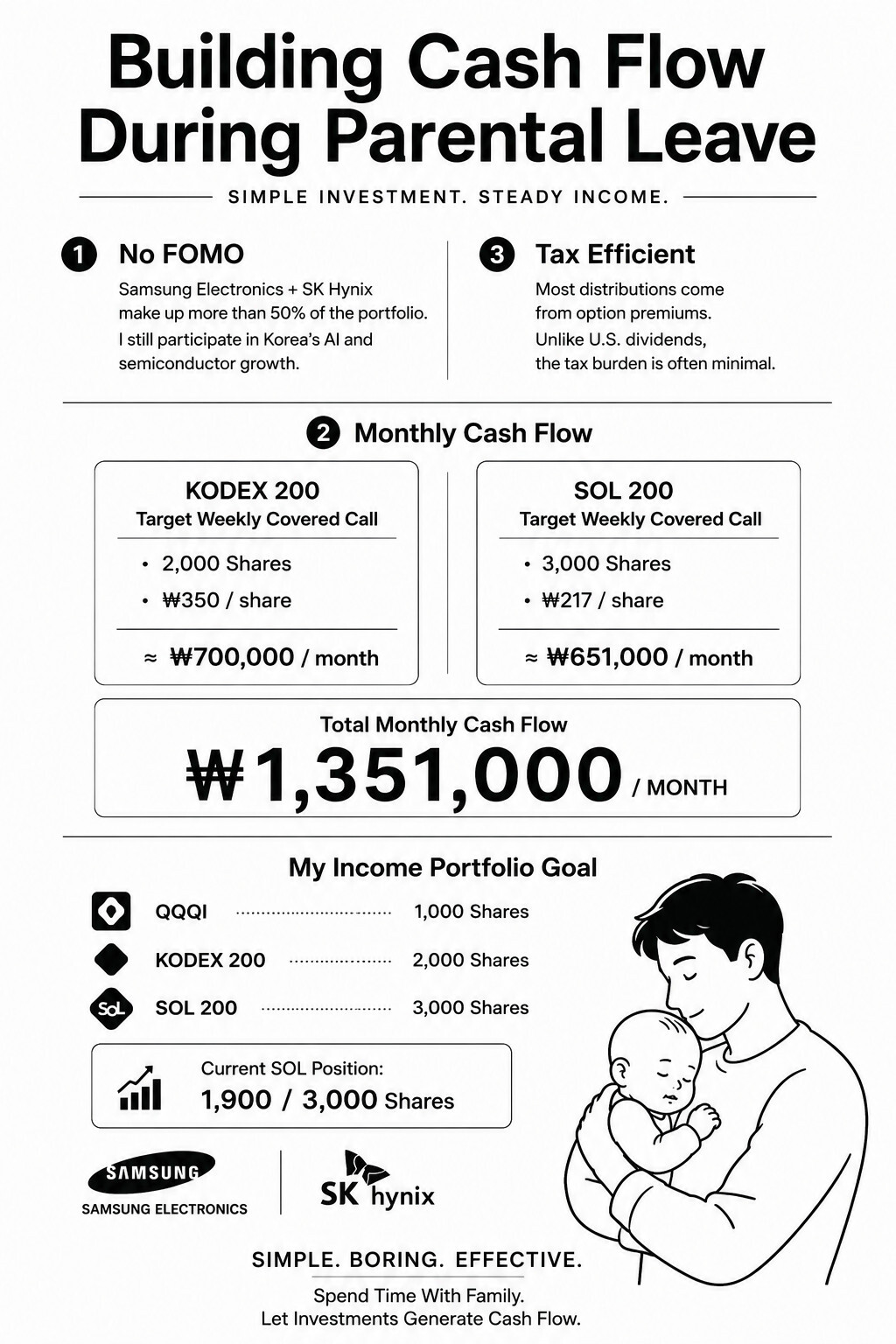

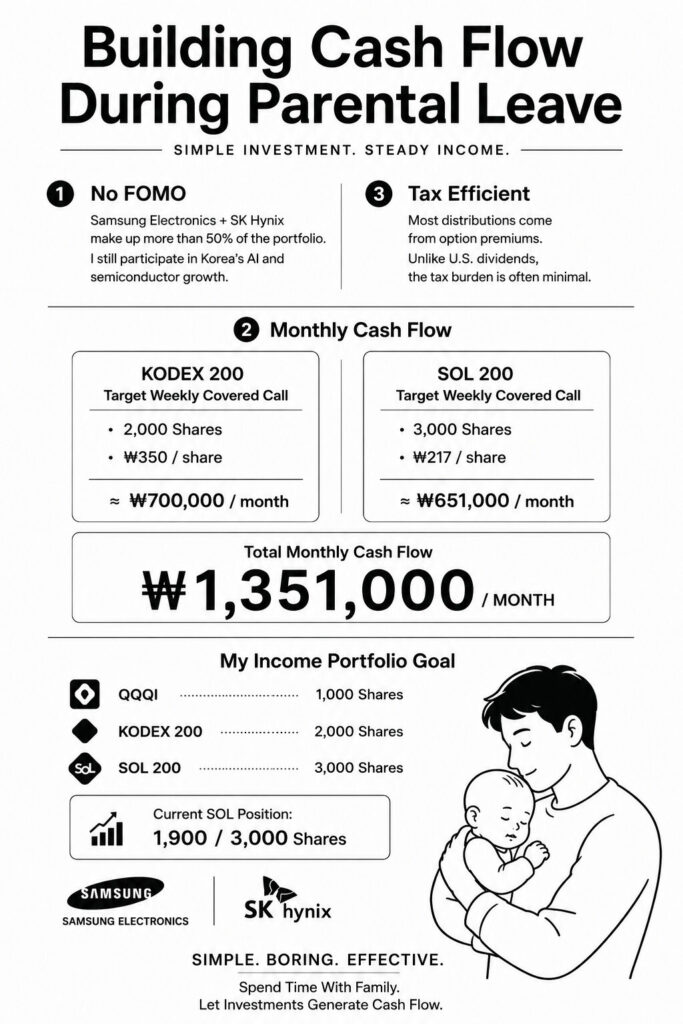

The second reason is the cash itself. These funds pay out monthly, and the numbers are real. In its first full year (2025), KODEX 200 Target Weekly Covered Call made 12 distributions totaling about 1,954 won per share — an annual distribution yield of roughly 14% against its net asset value. More recently, the June 2026 payout was about 350 won per share, while SOL 200 Target Weekly Covered Call paid about 217 won per share.

Here’s how that translates for my own targets, using those June 2026 figures. My target of 2,000 shares of KODEX, at about 350 won per share, would generate roughly 700,000 won a month — about $465 (at roughly 1,500 won to the dollar). SOL paid about 217 won per share, so my target of 3,000 shares works out to about 651,000 won, or roughly $435 a month. I’m at 1,900 SOL shares right now, which already brings in around 412,000 won — about $275 — each month while I keep accumulating. Fully built, the two funds together would produce roughly 1.35 million won, about $900 per month, in Korean covered-call income, sitting alongside the dividend from my 1,000 shares of QQQI on the US side. (Distributions vary month to month with market volatility, so I treat these as ranges, not promises.)

For a family living on a single income during leave, that monthly deposit landing without me doing anything is exactly the kind of buffer that lets me breathe.

Reason 3: A Remarkably Light Tax Burden

The third reason is the one most foreign readers find surprising, and it’s my favorite. Most of what these ETFs pay out comes from option premium, and in Korea, the option-premium portion of the distribution is effectively tax-exempt.

The real numbers make it vivid. In one recent month, of a KODEX distribution of about 262 won per share, roughly 84% came from weekly call-option premium — which carries no dividend income tax — while only about 16% (the part derived from the KOSPI 200 stocks’ actual dividends) was taxable. In one widely-cited example, an investor holding 1,120 shares received about 293,000 won but paid only around 5,600 won in tax — an after-tax retention rate above 98%.

Contrast that with US dividends, where a Korean investor faces about 15% withholding right off the top. The gap is enormous. And for me, this isn’t just about keeping more money — it’s strategic. Because I work hard to keep my total financial income under Korea’s 20-million-won threshold (to avoid comprehensive income taxation and extra national health insurance charges), a distribution that’s mostly tax-free lets me collect far more cash before bumping into that ceiling. Tax efficiency here directly protects my health-insurance status. That’s a quiet but powerful advantage.

My Parental-Leave Accumulation Plan

True to my project-manager habit of setting clear milestones, my Korean income plan is simple and concrete:

- QQQI: 1,000 shares — already reached (my US-side income anchor).

- KODEX 200 Target Weekly Covered Call: 2,000 shares.

- SOL 200 Target Weekly Covered Call: 3,000 shares — currently at 1,900 and accumulating.

Spreading across two providers (Samsung’s KODEX and Shinhan’s SOL) also diversifies my pipeline rather than leaning on a single fund.

The Risks I Keep in Mind

Honesty matters, so here’s the other side. In a powerful bull run, these covered-call ETFs will underperform a plain KOSPI 200 index fund, because selling calls caps part of the upside. The distributions are not fixed — they rise and fall with market volatility and option premiums. And the option income does not protect you from losses in the underlying stocks: if the KOSPI 200 falls, the fund’s net asset value falls too, just like any equity investment. These are income tools, not safe-haven assets, and they carry real market risk.

Final Thoughts

For me, KODEX and SOL 200 Target Weekly Covered Call hit a rare trifecta during parental leave: built-in exposure to Korea’s biggest stocks so I never feel left out, steady monthly cash to cover real life, and a tax structure so light it barely registers. That combination is why these two Korean covered call ETFs anchor my won-denominated portfolio while I focus on what matters most right now — my family.

Investment & Tax Disclaimer

This article reflects personal experience and opinions only. It is not financial, investment, or tax advice, and I am not a licensed financial advisor or tax professional. Distribution figures are based on past payouts and will change; past distributions do not predict future ones. Covered-call ETFs carry real risks, including capped upside in rising markets, variable distributions, and loss of principal if the underlying index falls. Tax treatment depends on your individual circumstances, account type, and current law, all of which can change — verify details with Korea’s National Tax Service and a qualified tax professional. All investing carries the risk of loss, including the loss of your entire principal. Please do your own research before investing.