2026 Stock Market Outlook: 3 Things That Will Drive US Stocks in the Second Half

After June delivered a short, sharp pullback in semiconductors and tech, the market has felt a little stuck. Following a year that kept setting record highs, profit-taking and a pile of external variables left investors fatigued. But when I synthesize the 2026 stock market outlook from major global investment banks like J.P. Morgan, Morgan Stanley, and Goldman Sachs, the consensus message is clear: stay “constructive, not complacent.” Below are the three things I’ll be watching to gauge where US stocks head in July and the back half of the year — plus a roundup of what other analysts are saying, and an honest note on my own (rough) June.

The Setup: A June Breather After a Record-Breaking Run

Let me set the scene. Stocks ran hard from the start of 2026, and after that kind of climb, a digestion phase was almost inevitable. Profit-taking in the leadership names and a cluster of macro worries combined to cool things off. Yet the big banks haven’t turned bearish — they’ve turned careful. That distinction matters, and it frames everything below.

1. A Powerful AI Capex Cycle and an Earnings-Driven Market

Even with the recent wobble, the engine under this market — corporate earnings — remains remarkably strong. The AI-driven capital-expenditure cycle in data centers and power infrastructure is still growing explosively. S&P 500 earnings are expected to rise somewhere around 23–25% across 2026, and on the strength of that, strategists are recommending an overweight to US equities relative to the rest of the world.

The numbers behind the AI buildout are staggering. Goldman Sachs estimates the largest hyperscalers will spend roughly $754 billion on capex this year — an 83% jump from 2025 — and expects AI-infrastructure beneficiaries to account for about half of all S&P 500 earnings growth in 2026. When earnings grow like this, valuations that look high can stay supported. This is, above all, an earnings-driven market.

2. Energy-Driven Inflation and a Fed on Hold

The biggest weight on the market is the familiar pair: inflation and interest rates. Recent geopolitical tension in the Middle East — including disruption around the Strait of Hormuz — has driven energy-price volatility and rekindled inflation worries. In response, the Federal Reserve held its policy rate at 3.50%–3.75% in June.

The market has shifted away from betting on near-term rate cuts and toward the view that rates may simply stay put for a while. That changes the playbook: July won’t be carried by the macro tailwind of cheaper money. Instead, stocks will be ruthlessly differentiated by how much money companies actually earn. Fidelity has flagged the same risk from the other direction — if oil stays north of $100 and the energy shock proves stickier than the market hopes, it could push rates and inflation higher and pressure both stocks and bonds.

3. A Surprisingly Resilient US Economy

Here’s the cushion. Despite higher-for-longer rates and an energy shock, the US economy is projected to grow at a solid ~2.1% this year. The labor market has stayed relatively stable, and consumers still have spending power. That resilience acts as a powerful floor — a downside-rigidity that makes a market collapse far less likely even when sentiment sours. It’s the quiet reason the big banks can stay constructive.

What Other Analysts Are Saying

Since I wanted a fuller picture than any single house, here’s how a range of strategists are framing the second half:

- Goldman Sachs raised its year-end 2026 S&P 500 target to 8,000, with 2026 EPS around $340 (about 24% growth). It stays constructive but waves two caution flags: narrowing market breadth and a sharp run-up in momentum.

- J.P. Morgan is firmly in the bull camp, describing the US as the world’s growth engine, driven by a resilient economy and an AI-driven supercycle that’s fueling record capex and rapid earnings expansion.

- Charles Schwab notes that earnings have defied nearly every cautious forecast (full-year growth now pegged near 25%) — but adds a sobering reality check: under the surface, the average S&P 500 stock has already suffered a max drawdown of around -21% this year, and historically, years with 20%+ earnings growth have produced surprisingly modest index returns as investors doubt the pace can last.

- Fidelity thinks the bull run stays intact — even hinting at a possible AI-driven “melt-up” — as long as investors keep their focus on earnings rather than the energy headlines.

- CIBC’s Christopher Harvey strikes a more measured tone, looking for a more modest ~8.8% gain on the year, with risks ranging from credit markets to skepticism about returns on AI spending.

Put it all together and the consensus is coherent: constructive but selective, with elevated valuations (a forward P/E near 21x) and narrow leadership as the main things to respect.

My July Strategy

Translating all of this into a plan, here’s how I’m approaching July:

- Focus on Q2 earnings. The second-quarter reporting season kicks off in mid-July, and the quality companies that raise their forward guidance are the ones likely to lead. In a differentiated market, guidance is everything.

- Consider diversification. With US mega-cap tech valuations stretched (that ~21x forward P/E), analysts suggest preparing for volatility — whether through inflation-hedging real assets or by spreading into other sectors and regions where earnings growth stands out. I treat my income ETFs as ballast for exactly this reason.

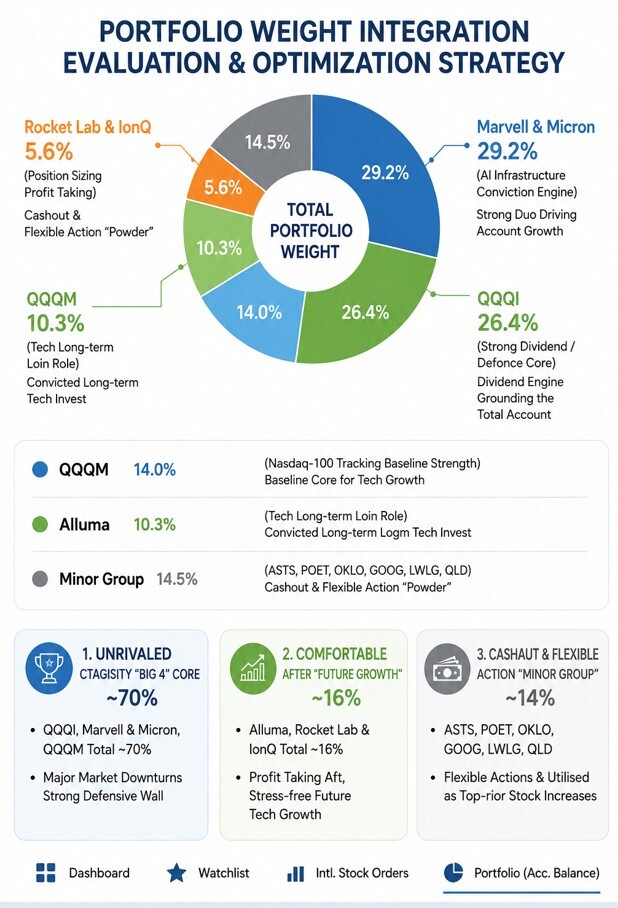

My Personal Position Going Into July

I’ll be transparent, because that’s the point of this blog. In early June, I partially raised cash — and then used some of it to add a bit more Rocket Lab and IonQ to my speculative growth sleeve. June was honestly a rough month for me: my account fell about 10%. That stings. But that’s also the nature of investing through a digestion phase after a huge run. With July starting next week, I’m hoping it’s a month full of good news — and I’ll be watching those Q2 earnings closely to see whether the constructive case holds.

Final Thoughts

The 2026 stock market outlook for the second half boils down to a single idea: the easy, everything-rises phase is probably over, and a more selective, earnings-driven market is taking its place. Strong AI capex and a resilient economy provide real support; sticky energy inflation and rich valuations demand respect. Constructive, not complacent — that’s the stance I’m carrying into July.

Investment Disclaimer

This article reflects personal opinions and a synthesis of publicly reported analyst views — it is not financial, investment, tax, or legal advice, and I am not a licensed financial advisor. Analyst forecasts and price targets are frequently wrong, and the holdings I mention describe my own portfolio, not recommendations. Markets can fall sharply regardless of any outlook. Past performance does not guarantee future results, and all investing carries the risk of loss, including the loss of your entire principal. Please do your own research and consult a qualified, licensed professional before making any investment decision.